Take Back Retirement

Episode 39

Do You Need a Financial Advisor?

“I’d like to work with a financial advisor, but I just don’t have enough money.”

Sound familiar? It’s a common objection when it comes to that all-important decision to get help in managing your money. But to this, Stephanie and Kevin have only this to say:

“But you have questions. Therefore, you need answers.”

Remember, there are no one-size-fits-all strategies when it comes to money advice. The most important first step is to figure out what you’re hoping an advisor can do for you.

Listen in as Stephanie and Kevin share the three questions you must answer if you’re considering hiring a financial advisor, the real value of having the right advisor, and what to do if your current advisor is unable to offer you the relevant information you need in your present circumstances.

Please listen and share with your friends who are in the same situation!

Key Topics

- The three questions to ask if you’re thinking of hiring a financial advisor (2:40)

- “What are you hoping an advisor could do for you?” (5:10)

- “I don’t help people save money. I help people spend money.” (7:02)

- Why you should ask your potential advisor how they get paid (9:28)

- A financial advisor helps you ask smarter questions (11:25)

- The value of an advisor (14:26)

- The right approach to investing (17:30)

- Is it time to let your current advisor go? (23:20)

0:06

Stephanie McCullough: Welcome to Take Back Retirement, the show for women 50 and better, facing a financial future on their own. I’m Stephanie McCullough, and along with my fellow financial planner, Kevin Gaines, we’re going to tackle the myths and mysteries of “Retirement,” so you can make wise decisions toward a sustainable financial future. Through conversations and interviews, you’ll get the information and motivation you need, to move forward with confidence. And we’ll be sure to have some fun along the way. We’re so glad you’re here. Let’s dive in.

0:39

Kevin Gaines: The other day, waiting to pick up my dog from doggy daycare, I was talking to another dog parent. And she mentioned, “I’d like to work with a financial advisor, but I just don’t think I have enough money.” Now, we’d had a five-minute conversation of all the things that are concerning her, and I just looked her in the eyes and said, “But you have questions. You need answers.”

1:08

Stephanie: Coming to you semi-live from the beautiful Westlakes Office Park in suburban Philadelphia, this is Stephanie McCullough and Kevin Gaines of Sofia Financial and American Financial Management Group. Say hello, Kevin.

1:19

Kevin: Hello Kevin.

1:20

Stephanie: So, today we’re talking about how to decide whether to work with a financial advisor or not. And the story that Kevin told me and just told you, is really what brought this up because we hear this a lot. I hear women say, “Oh, maybe when I have some investments, I can hire you.” But they’re still trying to figure out whether to refinance their house, and how to deal with their employee benefits at work, and what their divorce means for their retirement options. These are all financial advisor questions.

1:54

Kevin: And there is no absolute, one size fits all answer. There isn’t. There are plenty of people, plenty of you listening to this, don’t need to work with a financial advisor. You’re just looking for more sources and more thoughts and everything and that’s all you need, maybe. And there’s a lot of others that are saying, “No, I need help. I just don’t know who to go to or if I should go to” or, as I talked about in the opening, I don’t have “enough money,” which is a ridiculous reason not to at least think about if you need an advisor.

2:33

Stephanie: Well, Kevin, you have these three questions that you suggest people ask themselves when they’re thinking about it. Why don’t you share those three questions?

2:40

Kevin: I was at a conference several years ago. Stephanie, I think you were at this conference. And somebody stood up, did a presentation and when he said these words, that heavens opened up to me, it’s like, oh my gosh, this is it. And this is three questions for life, not just for financial advisors. Anytime you want to think about a contractor or anything, ask yourself these three questions. And you may already be doing this. Question one. Can I do this myself? Two. Will I do this myself? Three. Is this the best use of my time? Or to phrase it another way, is this what I want to be doing? So, I have a yard. I have a lawn mower. I can mow the lawn myself. I’ve been mowing the lawn myself since I bought my house. So, I definitely will do it. Is it the best use of my time? I actually enjoy mowing the lawn so yes, it is.

3:46

Stephanie: But you went through the process, and you ask yourself the questions.

3:49

Kevin: Exactly. Every so often, my wife says, “Do we just want to hire someone?” “No, I enjoy doing this.” Now, somebody else? A particular person I’m picturing, yes, he can do it himself. Yeah, he would. But truthfully, between his car and being a golf nut, that is not the best use of his time. Right? So, he pays, whatever he pays to have the local boy come by and mow the lawn and handle all the other stuff. Again, asking the three questions and at different spots.

4:24

Stephanie: And I have an example of this, a real-life example. I talked to a woman, we actually did a paid consultation last year and she is a very capable, smart professional. She’s in the medical field, she had gone through a divorce. In the past, she had managed her own portfolio. She’d picked her own investments, she’d adjusted it, she’d done all that kind of stuff. So, the can I do it? The answer was absolutely, yes. However, nine months after we originally met, she reached out this week and said, “I’m so busy, I’m so stressed with my job, when I get home, this is not what I want to be doing.” The will I do it is not happening. “So, I need you to help me.” Absolutely. Awesome. I think that’s a worthwhile perspective to take.

The other thing I tell people to ask is, what are you hoping an adviser can do for you? Because there’s a range of financial advisors. That’s one of the problems with our industry, frankly, one of my gripes with it. You can’t tell what services an advisor provides by what they call themselves. They could be investment advisor, wealth manager, asset manager, financial advisor, financial planner, we can call ourselves whatever we want. That’s a problem.

5:42

Kevin: There is no legal definition for any of these titles we use. I think we’ve covered this in a previous episode. Don’t ask me which episode number. We’ve talked about a lot of the letters after our names, there are legal or regulatory parameters for defining those. But I could just call myself “God’s Gift to Finance” as my title.

6:09

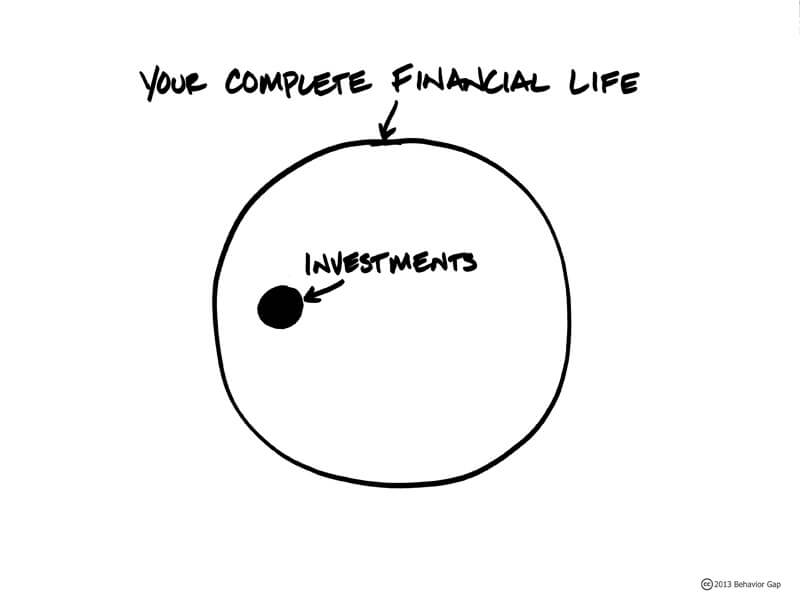

Stephanie: I could be “Queen of the World,” as long as compliance approved it on our business cards. There’s no legal standard. But I think another point came up, Kevin, in the story that you were sharing too, the questions we help clients with are not just about investments. We’ve got a graphic from our friend Carl Richards that we’ll share in the show notes that talks about your financial life is a very big circle and your investments are one small circle inside of that. Investing one’s money is one financial question, certainly, it is not the only financial question we face. And at least, how Kevin and I see it, financial planning is the term that we use to mean investments and all that other stuff.

7:00

Kevin: That’s actually a good point. For example, a little self-promotion here, I don’t help people save money. I don’t help people invest. That’s part of my job, don’t get me wrong. What do I do? I help people spend money. I concentrate on working with people who are on the verge are already in retirement. The question isn’t how to accumulate more money at that point. The question is, how do I spend that money? If you’re 20, 30 years old, just starting your family and everything? Yes. Would I be a good financial advisor for you? Yeah, but you know what, I could probably give you the names of 20 others that would probably do a better job because they specialize in talking about those situations. And frankly, to paraphrase JFK, ask not what you can do for your financial advisor, but what can your financial advisor do for you?

8:02

Stephanie: That was bad. That was bad.

8:05

Kevin: Always testing out other little taglines or quick little witty things to say and little peek behind the curtain. What you guys don’t understand is you only ever hear the little witticisms that I claim to come up with, you only hear about 10% of them. The other 90% Stephanie just sits there and go, “What the hell are you talking about?”

8:28

Stephanie: They get cut. They get left on the cutting room floor.

8:32

Kevin: Yes. This one I snuck in without testing it.

8:39

Stephanie: But Kevin, before we got on, you were talking about something that I think is important to share with our audience. And that’s that, if you’re looking at what advisors do, there are some financial advisors who really only do the investment management, they’ll invest your money for you, and they don’t really talk about the other stuff. And we’re not saying that’s bad, that is a perfectly legitimate business model. That is fine. You just want to know what you’re getting into. And on the other side, there are advisors who don’t do investments. They only do the financial planning and the other questions, and they’ll ask you to open an account at Vanguard or have your investments elsewhere. And of course, there’s everything in between. So, it’s understanding you know, what the advisor that you’re talking to does and what services they provide. That’s what you want to know and the other question you have to ask, and I promise you, it’s not a rude question, ask [is] how they get paid. Because that varies widely in our industry, it’s important to know, especially if you’re not physically writing a check or having a withdrawal from your account to the adviser. They’re getting paid somehow. So, understanding that is an important piece of the puzzle.

9:56

Kevin: Again, nothing nefarious is necessarily going on correct referencing the financial planners that only designed financial plans for you. They’re obviously not going to charge you for the assets under management because they’re not managing your assets. So, they’re going to be looking for maybe a one-time fee or a recurring fee, subscription model, something along those lines. Somebody who’s managing your assets, and that’s all they do, there’s nearly 100% chance that they’re going to be charging you based off the money under management, whether it’s what’s a fairly standard now in our industry, the AUM model, assets under management and they charge a percentage. Or do they charge transactions? If you think of the old-line stockbrokers, every time you buy and sell.

10:49

Stephanie: I think that’s common, because there is this, I meet people out and about, and they say, “Oh, yeah, I don’t have enough to invest with you.” I think this is where this comes from. Because advisors, firms that only make money on the money you’re investing with them, they often have minimums. So, “we only work with clients who have a half a million dollars to invest with us,” or higher, there’s certainly firms that have higher minimums. So that’s why you want to understand how people are getting paid, how they charge, because that’ll help you figure out if they might be a good fit for you. But there’s other questions too.

11:23

Kevin: Well, let’s not even say, next question, let’s pick up on that word question. Because what a financial advisor is going to help you do is ask smarter questions, we’re not going to tell you, or at least we shouldn’t be telling you what to do, unless you need that. And again, you can find an advisor that will do that. We’re going to help you ask smarter questions, we want to help you think through what’s going on. So, getting back to do I need a financial advisor? If you got a good grasp on all this stuff, already, you know exactly what you want to do you want to know how you’re going to get there, then, working with a financial advisor full time may not be the ideal situation for you. Periodically talking with one just as a quick check-in? Yeah, but you may not need one in that situation.

12:15

Stephanie: Several of my clients are women on their own, that’s kind of my specialty, women who are widowed, women who are divorced. And because we still live in this world where it’s not polite to talk about money or it could be uncomfortable to share with your friend or your neighbor or your cousin how much you have in the bank, whether you think it’s too much or too little, it might be uncomfortable. For a bunch of these clients, I’m the only person they can talk to about money. Whether it’s can I afford to renovate the kitchen? Can I afford to support my adult child? Am I going to have enough to support me the rest of my life? Or do I have to leave this home in this community that that I love? These are big questions, and they’re hard and stressful to wrestle with on one’s own. So really, I feel like a big part of our role is that decision making partner, that thought partner, sometimes accountability partner, if cuts to spending need to be made, or there does need to be some saving going on or that kind of uncomfortable stuff. Heck, just getting your will updated. I always say half my job is to nudge people to remind them to do that stuff that they really don’t feel like doing. Being that kind of partner to talk about money, I feel like that’s a big part of what we do, as well.

13:39

Kevin: I had somebody who summed it up very succinctly for me a few years ago. And again, I’ve loved this quote ever since because. He goes, “Kevin, listen. Here’s what I want you to do. I need you to help me figure out my goals. I need you to help me stay focused on these goals. And most of all, please stand between me and stupid.” Not everybody likes that, especially that last part, not everybody likes that particular quote. But since it was actually said, I feel safe and saying, “Hey, you know…”

14:16

Stephanie: And those tend to be your people.

14:18

Kevin: Those tend to be my people. A little bit more casual.

14:23

Stephanie: But I think that’s a big piece of it. And there have been studies on the value of an advisor. Vanguard does them every year, I think Russell Investments does, and they come up with trying to quantify the value. But one of the pieces of value that they have listed is helping clients avoid the big mistake. And that might not be something that you see every quarter or every year. I had one client who was really sold on investing quite a lot of money into her friend’s brand-new business and we talked about it. And we kind of talked her down a little bit. And again, I helped her ask good questions, I helped her come up with a list of questions to ask about the investment and in the end the opportunity fizzled out before she had to make a big decision. But again, trying to help people think through and avoid the big mistake. Another big mistake people often make is claiming their social security benefits too early. So, we understand social security, we know how the system works, we know all that. It’s complicated. No one teaches us that stuff in school, for goodness sakes. And even if they taught it to us in fourth grade, we wouldn’t remember by the time we were 62. So those kinds of decisions. If longevity runs in your family, and you’re still working, you probably you want to wait and claim your Social Security later. That’s the kind of stuff that has nothing to do with your investments. But that’s a big piece of what we do.

15:52

Kevin: Here’s the thing about Social Security specifically, is some people say, “Well, I can just talk to SSA.”

16:02

Stephanie: Social Security Administration.

16:03

Kevin: There I am with my initials again, anyway, assuming you can get through, or they just reopened the offices, so you can now go in person if you make an appointment. They’re not allowed to give you any advice. They can tell you, “This is the rule for this.” And they have default procedures that if you do this, then this is the order of things that they’re going to process or what they’re going to sign you up for. So, you can’t actually go to Social Security for help and advice.

16:33

Stephanie: Just facts.

16:34

Kevin: Just the facts, ma’am. Detective Friday, Sergeant Friday, sorry. So, you still want to have somebody to work with there. And again, there are some good resources on the internet that you can find, some really well thought of, intelligent professionals that have spent a lot of time talking about security. There’s also a lot of bad stuff out there as well. You got to be careful. I was having a conversation the other day, at a lunch at a chamber of commerce meeting, and lady came up to me afterwards and said, “Oh, you’ve said something about helping people while they’re in retirement. My husband just retired. He’s starting to ask questions about Medicare.” And I said, “Absolutely, we can have these conversations.” And she said, “Oh, good, because we have an investment advisor. But he only does investments, he doesn’t talk about this stuff.” And that gets back to one of our earlier points is not every professional is going to have the same conversations, the same focus. Different strokes for different folks.

17:45

Stephanie: And I would say, when you’re earlier in your career, the investment question is kind of simpler. Especially if it’s your retirement money, you’re just trying to sock away as much as possible and have it grow. It’s not as complicated and maybe doing it on one’s own or using a robo-advisor, one of these online systems, that can work. When you’re in what we call the accumulation phase, you’re adding to your assets, you’re building up your assets. But what we found both in the academic research and working with real human beings, is when you’re maybe five years out from retirement or some kind of change of life when you might be using some of that money you’ve accumulated, the investment question itself gets a lot more complicated. Because now it’s not all long-term money. Some of it is short term money, some of it you might be using in a year or two or three. Do we know exactly how much? Maybe, hopefully, we’re getting closer to an idea of how much you might be needing to pull out. But the other piece is, some of this is still long-term money. We just don’t know how long. So, it’s a very complicated question. In fact, I think on our episode on retirement income planning, we talked about this a bit, that it gets more complicated figuring out the right way to invest your money. And just a side note, very often if you have a 401k plan, there’s a target date retirement mutual fund in there, that’s gotten date. You pick the one that’s closest to when you think you might retire, you’re good to go. Yes, as you’re accumulating, but once you get closer to needing to use some of that money, I don’t think target date funds make sense, because they’re actually a single mutual fund, a single price, what’s called a net asset value. So, if you need to pull out $10,000, you’re selling a little bit of everything, as opposed to being able to kind of bifurcate the money into shorter term and longer term and only pulling out what’s up the most or what’s down the least or depending on market conditions.

19:52

Kevin: So, you see, there’s a different question. It’s not, what should I invest in? It’s not I have all these other questions about investing. It’s, how do I segregate my money to the stuff I’m going to need sooner than later and the stuff I’m going to need later than later? There are many people that when they reach the end of their retirement, shall we say, that they have a lot more money than they wanted to have because they were scared to spend it. Conversely, there’s people that run out, I mean, we’re not talking about medical issues or something like that. They just overspent. Or they just underspend. Remember that retirement is about enjoying the 20, 30, 40, 50 years of less responsibility, maybe not no responsibility. You get to live the life you wanted to have as a kid, but now you’re old enough to do all those things. But yes, you want to make sure that you’ve got enough money to do all that stuff. But you don’t want to sacrifice if you don’t have to.

21:06

Stephanie: And then, on the opposite end, there’s my friend, Phyllis, who a bunch of years ago, took her mother who I think was then 72, mother was widowed and needed to think about her money, Phyllis took her mother to an accountant that they knew to try to figure out how much of her savings she could spend each year. That was the question. And the accountant said, “Well, your life expectancy is 83.” So, he divided by whatever, 11 years and told her how much to spend. Phyllis’s mother is now 94 and her health is failing. And she was a child of the Depression, it nearly killed her to have to spend down her assets so she could qualify for Medicaid, because she didn’t have any money left, because she’d spent as the accountant had told her, so not the best advice.

22:03

Kevin: That’s the problem with averages, is 49.99999% of the time, you’re going to be above that line, and 49.99999 times you’re going to be below that line.

22:18

Stephanie: Yep, very few people are going to actually hit the average. So, what do you do? How do we manage that risk? The risk of dying too early and the risk of living too long. These are the things that we think about a lot and talk to our clients about.

22:35

Kevin: Note, at no point in this conversation have we really talked about investments, specifically you got to have these stocks, or you got to have these bonds or everything. We’re talking about all these other questions surrounding, which gets back to our original point. Whether you’d need to work with a financial advisor or not, the amount of money you have to “invest” shouldn’t be the primary driver of making that call, or interviewing advisors to see who you should be working with if you want to work with somebody. It’s all these other questions. Do you need help? Want help? And is it the best use of your time is figuring out these questions as well?

23:19

Stephanie: We’ve been talking about if you don’t have an advisor, and you’re thinking about whether or not to go hire someone, but there’s also, perhaps, people who have an advisor that maybe isn’t answering all the questions that they are looking for answers on. What would you be the thoughts there, Kevin?

23:38

Kevin: You may like your advisor, might even be a personal friend. So, you’re going to be hesitant to say, “You’re not helping me answer the questions I need answered today.” 10 years ago, perfect advisor, maybe a little less so now. Think of it this way. The house you have might be perfect for raising your family and having your kids, their friends come over, and you have pool parties and all that stuff. But as they move away, do you still need that house? Maybe you do. Maybe you don’t. It’s not saying it’s a bad house. It just doesn’t work for you anymore. That’s a question and, again, maybe you didn’t need an advisor in your 20s and 30s, or 40s, you had it all figured out, and it was simpler and everything. Again, as you get older, there are a lot more moving parts. Or maybe it’s like, I don’t have the patience for this crap anymore. Let somebody else worry about it.

24:45

Stephanie: I would also say if you’ve got an advisor, and there’s kind of a rhythm, there’s meetings, and they go through their agenda. I know people who have inherited advisors from their parents, from their ex-spouse or from their deceased spouse, and they’re still with the same advisor, don’t be afraid to ask the questions. Like, “Hey, Joe, thanks so much for your review of the markets and how the account has done. Can you help me think about Medicare?” Or “I’m really wondering how I should be approaching Social Security?” Or “What am I going to do with that old, you know, benefit I had from my previous job?” Whatever the question is, ask them, you’re paying them. I would say start there, come up with your list of questions, and see how that goes.

25:31

Kevin: Put a little less guilt aside, I have referred existing clients to other advisors because I wasn’t providing what they really needed. I wasn’t the best person for that. Typically, in my world, it’s the children come with me, but they start having things come up like, “You know what? I got this buddy over here. Why don’t you talk to him?” Or “She can really help you figure this stuff out. I’m not the best person.”

26:02

Stephanie: We don’t pretend to be all things to all people by any stretch. Not at all. We’d love to hear your questions. We’d love to hear your experiences in searching for an advisor. I have had people tell me that you can’t swing a cat without hitting 75 advisors in my area of the world. There are plenty of financial advisors out there. What have you seen? What has been your experience? Have you been out looking? Did you inherit someone from a previous family member? I’m curious, please hit us up on social media and tell us what you’re seeing. Or heck, you can go to the takebackretirement.com website, there’s a contact form there, send us a little note. We’re really curious to hear your experience. And maybe if you’ve got a good story, we’ll even have you on the show. Thanks so much for being with us. We’ll talk to you next time. It’s goodbye from me.

26:58

Kevin: And it’s goodbye from her.

27:02

Stephanie: Be sure to subscribe to the show and please share it with your friends. Show notes and more information available at takebackretirement.com. Huge thanks for the original music by the one and only, Raymond Loewy through New Math in New York. See you next time.

27:16

Disclaimer: Investment advice offered through private advisor group, LLC, a registered investment advisor. Private advisor group, American Financial Management Group, and Sofia Financial are separate entities. The opinions voiced in this material, are for general information only and are not intended to provide specific advice, or recommendations for any individual security. To determine which investments may be appropriate for you, consult your financial advisor, prior to investing. This information is not intended to be substitute for individualized tax advice. Please consult your tax advisor regarding your specific situation.